The Bank of Canada did not raise interest rates this week. Bullet dodged there but don’t expect the governments and powers that be to leave the market alone. We still have an affordability challenge. (really a supply challenge that’ll take a long time to solve, rather than a neat sound bite or a 4 year election cycle solution).

That’s not today’s story.

Where have all the listings gone? Remember a month or 2 ago how the media was crowing about all the variable rate mortgages hitting their trigger rates. The rate at which the monthly payment was no longer covering principal repayments and in some cases not even covering the interest payments. These zombie mortgages should have driven a ton of people to sell and flood the market with panic driven sellers. Hasn’t happened, at least not yet. That tells me consumers weren’t so leveraged that they didn’t have room in their budget to deal with an increased mortgage payment. It also tells me that for some the likely case is that they trimmed the budget elsewhere in order to add the increased mortgage payment. That means less consumer spending on consumables like eating out, or travel. ( a positive impact on inflation).Smart home buyers over the past 2 years had the foresight to anticipate rate increases and either held savings back to cushion any increase or like the generations before them were prepared to sacrifice other aspects of their budget in order to own real estate. That doesn’t mean some folks are in financial pain. There’s pain out there, no doubt. What I see is that those in pain are either prepared to work and live through it and reconfigure their budgets or they aren’t ready to throw in the towel just yet.

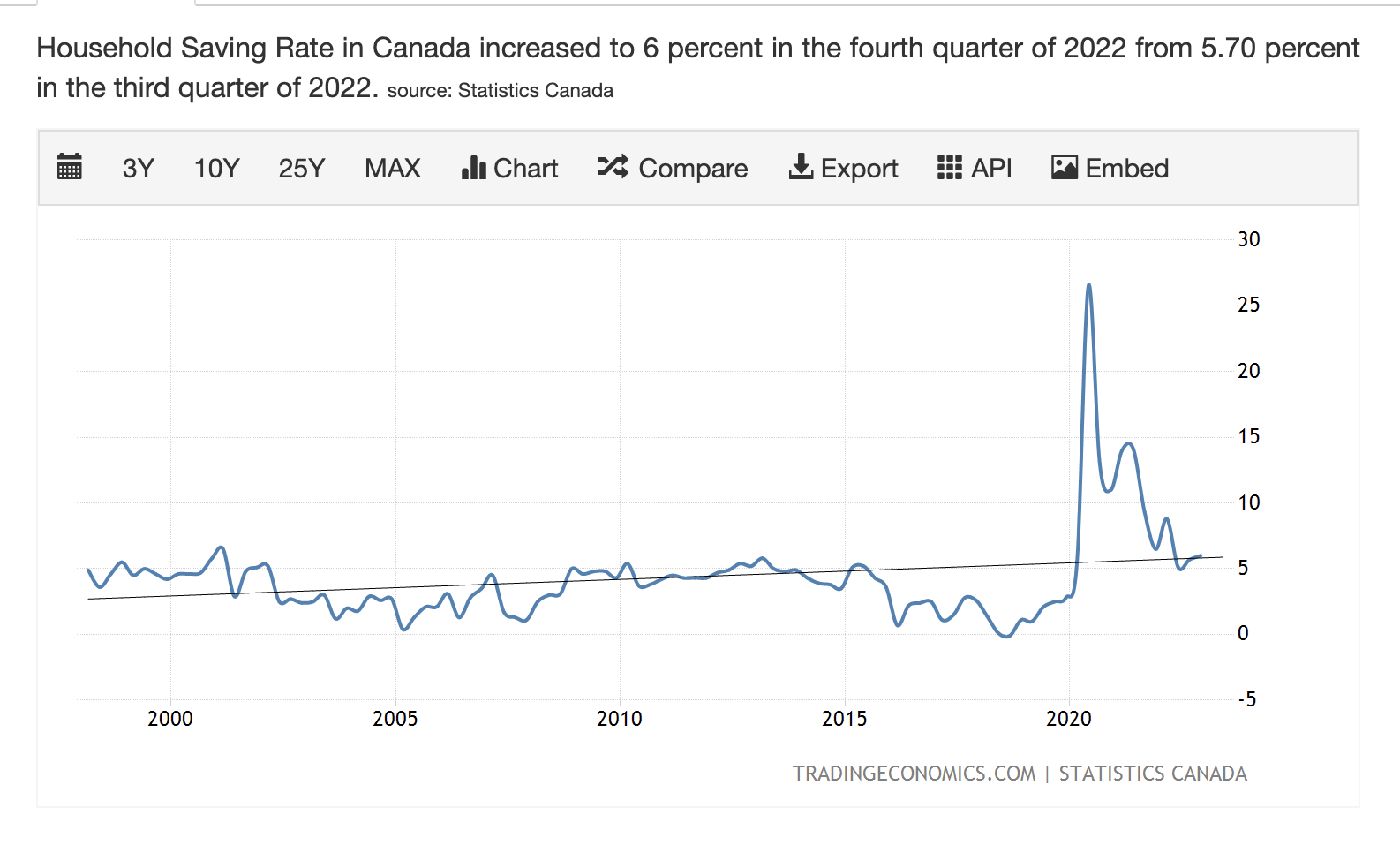

I did a bit of research through the Canadian Bankers Association. I was after a report on the delinquency rates for mortgages in Canada and Ontario specifically. The numbers are rather surprising! First let’s review how much Canadians have been saving. Prior to the pandemic and for the past 20 plus years the savings rate had been bumping along for the most part, just under 5%, with the trend line on a gentle upward slope.

The pandemic shows a massive spike in savings well over 20% as a result of the lockdowns where people couldn’t spend and wisely didn’t spend. If you were like me, you probably went through your budget and did a lot of slashing because you realized you didn’t need that spending or eliminated it because of what might or might not happen with the pandemic.

The savings rate is now above the trend line, that’s a good thing, which tells me people have built contingency plans into their budgets and continue to increase their savings. Yes, we did spend a lot after the pandemic but those funds went into durable consumer goods and services like renovations, additions and things like appliances. Long term spending to improve a long term asset.

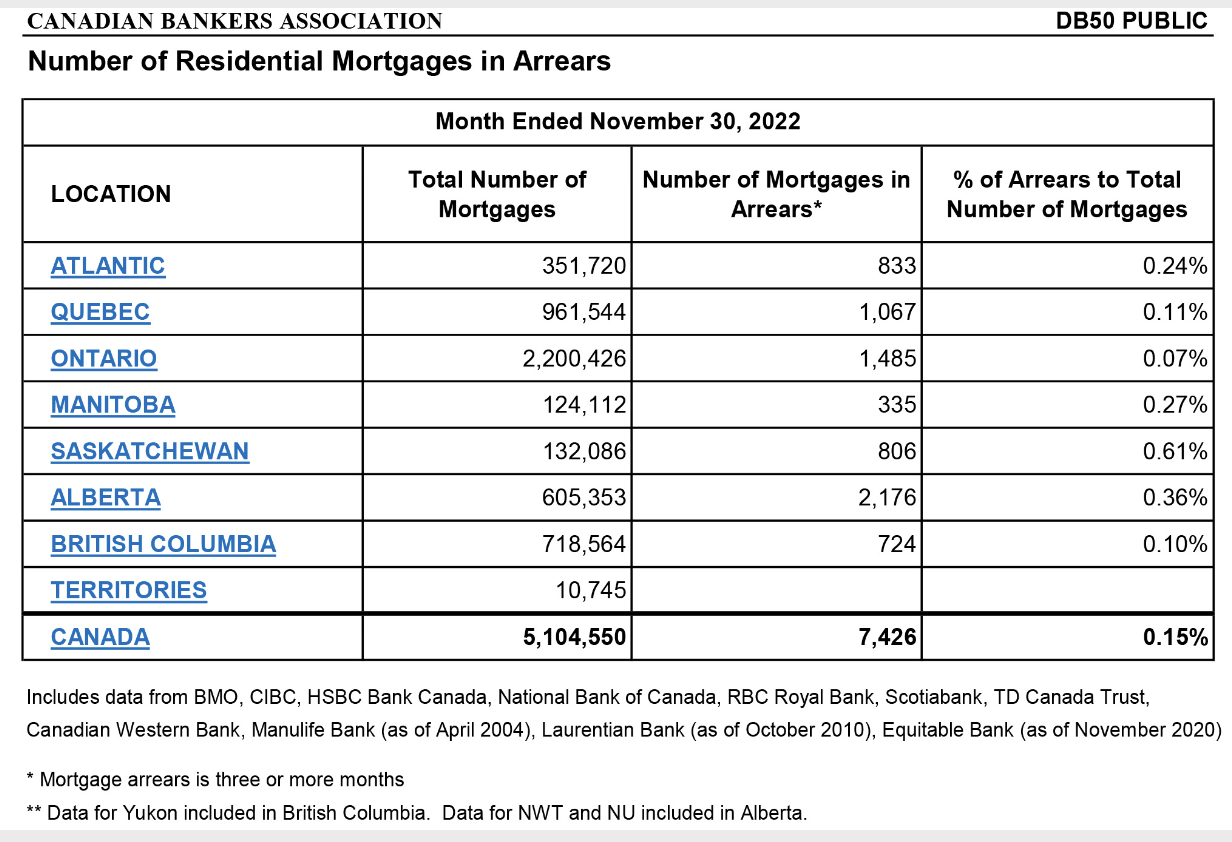

Now review the mortgage arrears data, within the perspective of a higher savings rate.

The chart above shows that in Ontario with 2.2 million mortgages only 1,485 or 0.07% are in arrears of 3 or more months. Note, what’s not included in these numbers are arrears figures from the majority of B lenders. Interestingly, between April 2020 and February 2021 the arrears rate in Ontario rose to a peak of 0.12% or roughly 2,400 mortgages at the height of the pandemic. For perspective, in the mid to late 1990’s the delinquency rate hit a high of 0.64% which was 6,400 mortgages out of 980,000. For those of you that don’t recall that time period, there was a lot of pain for homeowners, inflation had finally settled down and mortgage rates were finally dropping to under 10%. I’m not insensitive to the fact that these numbers represent real families that are struggling financially and some of those families will be in our community. Our message here is that, thankfully, the situation is not as bad as we have been led to believe. And this is why I believe we won’t be seeing a flood of listings entering into the marketplace. For those buyers on the sidelines waiting for blood to run in the streets, I think you’re going to be waiting and missing out on the existing opportunities that are available. Interest rates will not be returning to the low rates of 2 years ago and until supply of available homes picks up considerably I don’t expect this market to become a buyer’s market either. I guess what baffles me the most is that sellers are also parked on the sidelines and I’m not sure what they are expecting from the market, as most of the region is still considered to be in a balanced or slight sellers market. As close to “normal” conditions as I’ve seen in a while. Yet, consumers and even Realtors all seem to be milling about like a grade nine high school dance, waiting for someone else to move onto the dance floor. Don’t wait for Stairway to Heaven to start playing!

Enjoy what is hopefully the last gasps of winter weather this weekend. It’s the spring forward weekend. Most of our devices will do it automatically but you’re still losing an hour of sleep. The extra hour of sunshine should do wonders for the real estate market..

That’s not today’s story.

Where have all the listings gone? Remember a month or 2 ago how the media was crowing about all the variable rate mortgages hitting their trigger rates. The rate at which the monthly payment was no longer covering principal repayments and in some cases not even covering the interest payments. These zombie mortgages should have driven a ton of people to sell and flood the market with panic driven sellers. Hasn’t happened, at least not yet. That tells me consumers weren’t so leveraged that they didn’t have room in their budget to deal with an increased mortgage payment. It also tells me that for some the likely case is that they trimmed the budget elsewhere in order to add the increased mortgage payment. That means less consumer spending on consumables like eating out, or travel. ( a positive impact on inflation).Smart home buyers over the past 2 years had the foresight to anticipate rate increases and either held savings back to cushion any increase or like the generations before them were prepared to sacrifice other aspects of their budget in order to own real estate. That doesn’t mean some folks are in financial pain. There’s pain out there, no doubt. What I see is that those in pain are either prepared to work and live through it and reconfigure their budgets or they aren’t ready to throw in the towel just yet.

I did a bit of research through the Canadian Bankers Association. I was after a report on the delinquency rates for mortgages in Canada and Ontario specifically. The numbers are rather surprising! First let’s review how much Canadians have been saving. Prior to the pandemic and for the past 20 plus years the savings rate had been bumping along for the most part, just under 5%, with the trend line on a gentle upward slope.

The pandemic shows a massive spike in savings well over 20% as a result of the lockdowns where people couldn’t spend and wisely didn’t spend. If you were like me, you probably went through your budget and did a lot of slashing because you realized you didn’t need that spending or eliminated it because of what might or might not happen with the pandemic.

The savings rate is now above the trend line, that’s a good thing, which tells me people have built contingency plans into their budgets and continue to increase their savings. Yes, we did spend a lot after the pandemic but those funds went into durable consumer goods and services like renovations, additions and things like appliances. Long term spending to improve a long term asset.

Now review the mortgage arrears data, within the perspective of a higher savings rate.

The chart above shows that in Ontario with 2.2 million mortgages only 1,485 or 0.07% are in arrears of 3 or more months. Note, what’s not included in these numbers are arrears figures from the majority of B lenders. Interestingly, between April 2020 and February 2021 the arrears rate in Ontario rose to a peak of 0.12% or roughly 2,400 mortgages at the height of the pandemic. For perspective, in the mid to late 1990’s the delinquency rate hit a high of 0.64% which was 6,400 mortgages out of 980,000. For those of you that don’t recall that time period, there was a lot of pain for homeowners, inflation had finally settled down and mortgage rates were finally dropping to under 10%. I’m not insensitive to the fact that these numbers represent real families that are struggling financially and some of those families will be in our community. Our message here is that, thankfully, the situation is not as bad as we have been led to believe. And this is why I believe we won’t be seeing a flood of listings entering into the marketplace. For those buyers on the sidelines waiting for blood to run in the streets, I think you’re going to be waiting and missing out on the existing opportunities that are available. Interest rates will not be returning to the low rates of 2 years ago and until supply of available homes picks up considerably I don’t expect this market to become a buyer’s market either. I guess what baffles me the most is that sellers are also parked on the sidelines and I’m not sure what they are expecting from the market, as most of the region is still considered to be in a balanced or slight sellers market. As close to “normal” conditions as I’ve seen in a while. Yet, consumers and even Realtors all seem to be milling about like a grade nine high school dance, waiting for someone else to move onto the dance floor. Don’t wait for Stairway to Heaven to start playing!

Enjoy what is hopefully the last gasps of winter weather this weekend. It’s the spring forward weekend. Most of our devices will do it automatically but you’re still losing an hour of sleep. The extra hour of sunshine should do wonders for the real estate market..